Purpose: To help individuals and families pay for their health insurance. Here's how you qualify:

Regards, Vincent Reda & the staff at Mainline Insurance

1 Comment

Insurance companies will offer their programs:

There are two Health Benefit Exchanges:

Level of Plans on the Exchange (the Metallic Plans)

Individual Marketplace:

Many insurance companies although not advertised and disclosed openly, to hold down costs have created smaller networks of doctors and hospitals. Those providers will be paid less. It is easy to see why the networks are smaller. Participants in the exchanges should be prepared for the much tighter narrower networks. The insurers say that with a smaller number of doctors and hospitals they can offer lower cost policies and have more control over the quality of the health care providers. They also say that this is better than no coverage.at all. Health plans having narrow networks that exclude many doctors, may discourage patients with expensive pre-existing conditions who have established relationships with doctors. Basically saying they do not want patients who for medical reasons require a broad network of providers We will be ble to help you navigate to see which insurance company’s networks and plan design best works for you. We expect there to be a combination of large legacy insurance companies, new insurance companies and existing insurance companies looking to expand their geographical footprint all offering market rate plans. This comes about since everyone has to have health insurance or be fined.This should provide ample competition thus keeping rates stable. Regards, Vincent  Small Business Health Care Tax Credit

Finally, a break for small businesses. Purpose: To help small business and small non-profit organizations afford the cost of covering their employees. How Do You Claim the Credit?

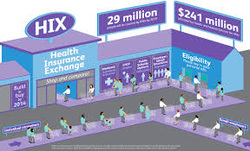

A key component in the new Affordable Care Act to help making healthcare affordable. Regards, Vincent and the Staff at Mainline Insurance  A major component of the Affordable Care Act is the Health Benefits Exchange.The Exchange is a tool for small businesses and individuals to obtain health insurance. We are prepared to help you navigate amongst the Business and Individual Exchanges along with the private market programs.

The Affordable Care Act comprises of two Exchanges.

Along with the Exchanges there will be regular market programs for additional benefit options. We are still waiting for guidance from the State concerning the rules and regulations. The first phase is to begin October 2013 for implementation January 2014. Note: the penalty for large employers (50+ on the payroll) has been pushed off till 2015 However: The penalty for employees still remains. Those employees will have to obtain coverage or be penalized. At Mainline Insurance we are prepared to deliver guidance to navigate during these changing times. Many employees that have to go to the Individual Exchange will receive subsidies from the government to help them afford their coverage. The education and certification process has started. Mainline Insurance has been certified and authorized to offer plans on the NYS Health Benefits Exchange. It appears it is taking the State some time to get the curriculum together along with the insurance companies still not delivering plan design and rates for plans offered on the exchange and in the private market. I anticipate the pace to pick up now since October is right around the corner. Stay tuned as the Affordable Care Act unfolds and we break it down for you. Regards, Vincent  We have entered the last quarter of the year and there are important items to discuss. This circulation addresses Emblem and HIP policyholders. Many of you have received notification that Emblem is terminating all plans for small groups effective 12-31-13. This also applies to groups that have Emblem through the LIA and HealthPass. Over the last several months we have brought notice of Emblem’s intention to leave the small group marketplace. In the future, Emblem wants to offer plans that are compliant with the Affordable Care Act. The irony Emblem’s current offerings are more than compliant already.

A transition will not be automatic and the industry does not know how Emblem will proceed with this change. As of the writing of this article, Emblem has not disclosed plan designs or rates for 2014. This same lack of information is concurrent across all insurance companies that offer plans in New York. I want you all to know that I am staying up to date on the situation. I hope to have a variety of options from Emblem and other providers shortly for review. Mainline will be able to illustrate and council on health insurance programs offered both on and off the Health Benefit Exchange. It appears there will be a larger selection of insurance companies offering plans in 2014. Under the Affordable Care Act, insurance providers that offer plans on the Health Benefit Exchange are also required to offer market rate plans off the Health Benefit Exchange. As I mentioned earlier, I will be keeping you informed. Please look out for our articles and newsletters. Mainline will be posting articles periodically detailing the Affordable Care Act and issues that are important to you. Please visit our website www.mainlineins.com to see articles previously posted. Regards, Vincent and the Staff at Mainline Insurance  The Affordable Care Act (ACA) requires employers to provide their employees with a written notice about exchanges to help explain some of the benefits and potential consequences associated with purchasing through an exchange. Employers must issue these notices as of October 1, 2013. We were just notified on Aug 28th, 2013. We thought an extension was in order.

The Exchange Notice must:

In order to provide your employees with the notification, please follow the link below to download the Employer Exchange Notification in PDF format. In order for employees to access the exchange they are required to fill out this form. Click Here To Download Mainline is certified and authorized to offer programs on the Health Benefit Exchanges as well as the private market plans. We are here to support our clients and friends. We encourage you to reach out with any and all questions as we transition into this new healthcare system. Best Regards, Vincent Reda & Mainline Staff  Yes it will. For businesses with under 50 Full time eligible employees on the payroll: you can purchase plans on the Small Business Health Options Program Exchange or purchase coverage through the regular non exchange marketplace. You are not obliged to provide coverage to the employees under the Health Care Reform Act. If you offer coverage and your employees do not participate and go on your plan we will then obtain coverage for them on the Individual Exchange to avoid penalties. For businesses with over 50 full time eligible employees on the payroll: you cannot purchase plans on the Small Business Exchange. In NYS there is conversation they will raise that threshold to 100 employees in 2017. Recently as of July 2013 they repealed the penalty for large groups (50+ full time on the payroll). No penalty will be imposed if they do not provide affordable healthcare to employees. The penalty will be reactivated in 2015. The penalty is $2000 per employee. The first 30 employees are forgiven, after that its $2000. The penalties’ will increase over time. For individuals: if you do not obtain health insurance from your employer you will have to obtain it on the exchange. If you do not obtain coverage you will be faced with a penalty. The penalty is $95 or 1% of your w2 wages. The penalties’ will increase over time. Stay tuned as the Affordable Care Act unfolds and we break it down for you. Regards, Vincent Mainline Insurance

Finally, the rates and plan designs for the health insurance plans to be offered on the New York State Health Benefit Exchange has been released. Policies vary based on guidelines set forth by the Federal government under the Affordable Care Act. This comprises of two exchanges; one for the Individual (non-business) and the other for Small Businesses with 2-50 employees.

Click Here To Download New Rates (PDF) We are still awaiting guidance from New York State concerning different rules and regulations. A comprehensive set off rules is scheduled for October of this year. On July 2, 2013, the Obama Administration announced on the Treasury Department’s website that it would delay the employer mandate for one year, until 2015. In the statement, the Administration said that they were delaying implementation in order to meet two goals: “First, it will allow us to consider ways to simplify the new reporting requirements consistent with the law. Second, it will provide time to adapt health coverage and reporting systems while employers are moving toward making health coverage affordable and accessible for their employees." Note, the employee mandate, which is a penalty for large employers (50+ on the payroll) has been pushed off till 2015. On July 2nd 2013 the Obama administration announced However, the penalty for the employees still remains. Those employees will have to obtain coverage or be penalized. At Mainline Insurance we will be well prepared to help. Many of these employees will receive an Advance Premium Tax Credit to help them afford their coverage. If any of you would like to have some discussion on this matter please feel free to call or email. The education and certification process for us to provide guidance is to start shortly. It appears it is taking the State some time to get the curriculum together. I anticipate the pace to pick up now since October is right around the corner. We will be keeping all of you well informed periodically. Regards, Vincent Reda Mainline Insurance  We at Mainline insurance will keep you up to date on the latest news in the healthcare industry. Following closely the new Affordable Care Act regulations and what they mean for your healthcare coverage.

|

AuthorMainline President Vincent Reda is a Healthcare specialist with 40 years of experience in providing healthcare coverage to individuals and organizations.

Categories

All

Archives

October 2018

|

||

RSS Feed

RSS Feed